In 2025-26 (April-March), India imported 28.2 million tonnes (mt) of fertilisers worth over $14.5 billion. That included 11.2 mt of urea, 6.4 mt of di-ammonium phosphate (DAP) and 3.7 mt of muriate of phosphate (MOP) valued at $5.2 billion, $4.9 billion and $1.3 billion, respectively.

The $14.5 billion import was more than the $8.2 billion for the previous financial year and the highest since the $15.3 billion of 2022-23.

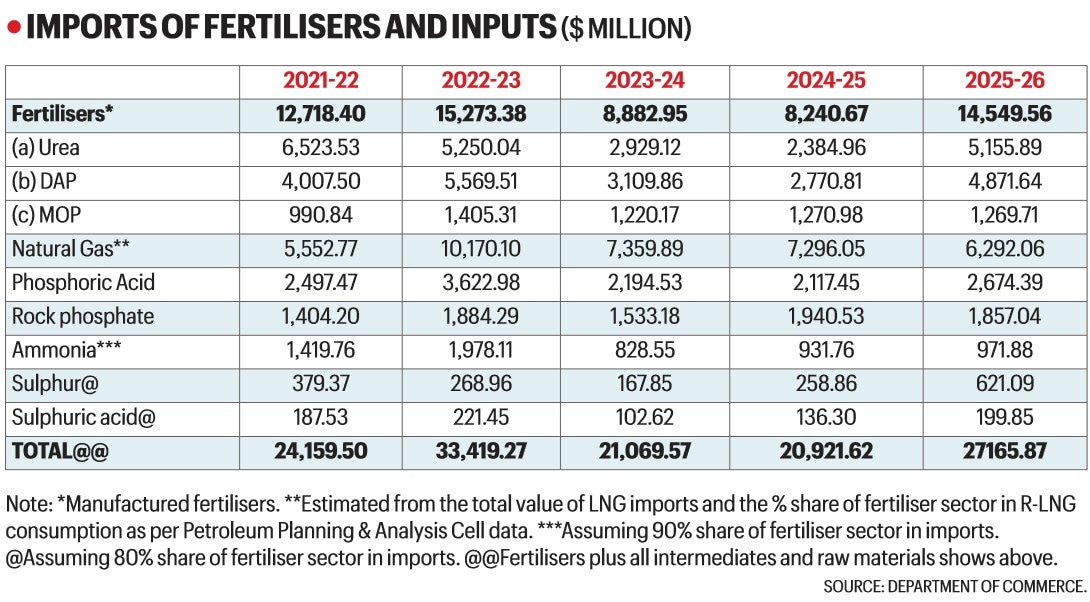

The above figures, however, pertain only to the import of finished fertilisers. They give an incomplete picture of the actual foreign exchange outflow from the country on account of fertilisers.

In 2025-26, India also produced 29.3 mt of urea, 3.9 mt of DAP, 12 mt of complex fertilisers containing nitrogen (N), phosphorus (P), potassium (K) and sulphur (S) in different ratios, and 5.7 mt of single super phosphate (SSP).

The domestic production of these fertilisers entailed use of intermediate chemicals or raw materials, which were imported.

Take urea, whose primary feedstock is natural gas. In 2025-26, India imported nearly 26 mt of liquefied natural gas (LNG) valued at $13.3 billion. According to Petroleum Ministry data, the fertiliser sector had a 47.2% share in the country’s consumption of regasified LNG last fiscal. The industry’s LNG imports alone would, then, have been worth some $6.3 billion.

The domestic manufacture of DAP is similarly based on imported phosphoric acid and ammonia. Some companies also manufacture phosphoric acid by reacting the raw material – rock phosphate, which is imported – with sulphuric acid. Sulphuric acid is, in turn, either directly imported or manufactured domestically by importing the raw material, i.e. sulphur.

Story continues below this ad

For the manufacture of complex fertilisers and SSP, too, the sources of N (ammonia), P (phosphoric acid/rock phosphate), K (MOP) and S (sulphuric acid/sulphur) are mostly imported.

The short point is that India imports more than half of its natural gas consumption requirement, while it has hardly any commercially mineable rock phosphate, potash or elemental sulphur reserves.

In 2025-26, India imported 2.2 mt of phosphoric acid (valued at $2.7 billion), 11.1 mt of rock phosphate ($1.9 billion), 2.5 mt of ammonia ($1.1 billion), 2.1 mt of sulphur ($776.4 million) and 2 mt of sulphuric acid ($249.8 million). An estimated 90% of the ammonia and 80% of sulphur and sulphuric acid imports was used for the manufacture of fertilisers.

The accompanying table shows that India’s total fertiliser import bill, inclusive of foreign exchange outgo on both finished products and inputs, was a whopping $27.2 billion in 2025-26, below only the record $33.4 billion for 2022-23.

Story continues below this ad

Table.

Table.

Impact of wars

In 2022-23, India’s fertiliser imports surge was due to Russia’s invasion of Ukraine. While it started on February 24, the real impact was in the fiscal year from April 2022.

One can expect the actual effects of the current United States-Israel versus Iran conflict, which technically began on February 28, to be felt in 2026-27. The West Asia crisis and closure of the Strait of Hormuz have already driven up global fertiliser prices.

India’s latest urea and DAP imports have been contracted at landed (cost plus freight) prices of $935-959 and $935 per tonne respectively, as against their corresponding year-ago rates of $410-420 and $725 per tonne. Landed per-tonne prices now of MOP ($383), phosphoric acid ($1,360), ammonia ($840-850) and sulphur ($750-850) are, likewise, way higher than their last year’s corresponding levels of $283, $1,055, $400-420 and $295-305 at this time.

Story continues below this ad

On top of the higher dollar-denominated import costs is the rupee’s depreciation. The dollar-rupee exchange rate was 95.7 on Friday, versus an average of 85.2 in May 2025.

The current landed prices of imported fertilisers are close to the highs during December 2021-September 2022 in the run-up to and immediately after the Russia-Ukraine war. These went up to $1,000-1,050 per tonne for urea, $950-1,000 for DAP, $590 for MOP, $1,715 for phosphoric acid, $1,575 for ammonia and $500-520 for sulphur.

If present trends hold, with no meaningful breakthrough in the ongoing US-Iran negotiations, India’s total all-inclusive fertiliser import bill in 2026-27 could reach or even cross the $33.4 billion record of 2022-23. The substantially weaker rupee makes it worse: The cost of higher imports is ultimately borne – whether by the exchequer, industry or farmers – in domestic currency.

Compounding the problem

Some state governments have recently issued orders banning the manufacturers and suppliers of subsidised fertilisers – urea, DAP, complex fertilisers, MOP and SSP – from selling any non-subsidised nutrient products.

Story continues below this ad

Uttar Pradesh was first to come out with such an order on January 13, followed by Madhya Pradesh on May 14 and Maharashtra on May 20.

The directives have caused disquiet in the industry. The bigger players – the likes of Indian Farmers Fertiliser Cooperative, Coromandel International, Yara Fertilisers India, Chambal Fertilisers & Chemicals and Paradeep Phosphates Ltd – sell both subsidised fertilisers (whose retail prices, movement and inter and intra state allocations are subject to government controls) and non-subsidised products (which are free from these regulations).

Non-subsidised products cover water-soluble fertilisers (such as sulphate of potash, mono ammonium phosphate and potassium nitrate, which can deliver nutrients straight to the plant’s root zone via drip irrigation), micronutrients (bentonite sulphur, chelated zinc and manganese, zinc oxide and boron powder), nano and liquid specialty fertilisers (suited for foliar application or spraying directly onto leaves), bio-stimulants (like seaweed extracts and carbon enhancers) and bio-fertilisers (including potash derived from molasses, liquid fermented or phosphate rich organic manures and microorganism consortia).

“These are premium fertilisers applied in low doses for high-value crops such as grapes, apple, banana, pomegranate, vegetables and sugarcane. They are sold through the same distribution and dealer channels as urea or DAP. While the subsidised bulk fertilisers bring in volumes, the non-subsidised speciality nutrients generate margins,” said an industry source.

Story continues below this ad

The state governments have justified the ban on cross-selling, citing allegations of companies resorting to “tagging” – forcing farmers to buy non-subsidised fertilisers along with subsidised fertilisers. “This would basically open the doors for fly-by-night operators pushing low-quality products without any proper farmer training and education,” the source noted.

The non-subsidised nutrient products sold by fertiliser companies are all approved and notified under the Centre’s Fertiliser Control Order, 1985. “We have a global supply crisis in bulk fertilisers and Prime Minister Narendra Modi himself has called for reducing their usage. The states are doing the opposite, by telling us not to sell products that have 80-90% nutrient use efficiency, as opposed to the 30-35% in conventional chemical fertilisers,” the source added.